"There are literally hundreds, if not thousands, of articles trying to assess and address the impacts of COVID-19 on the construction industry; and there are more being published every day."

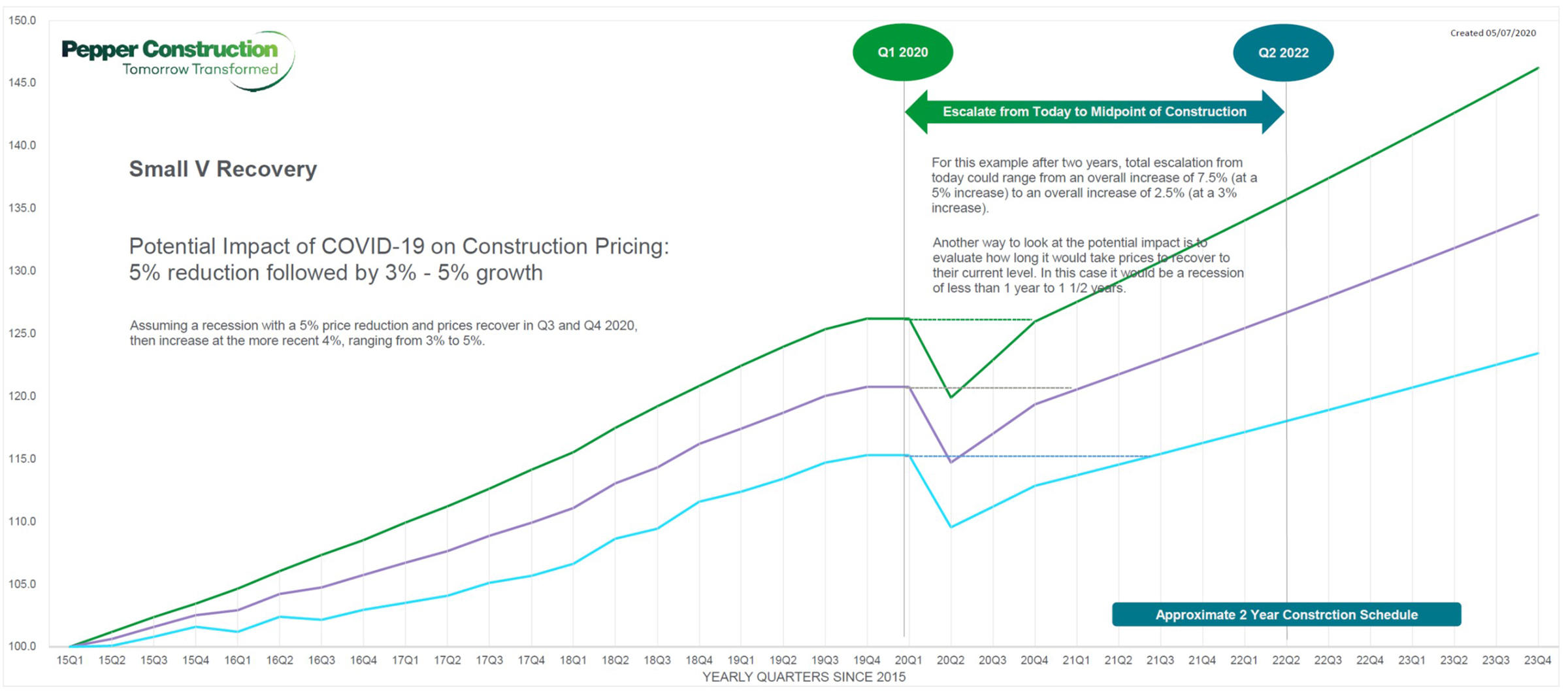

Senior Vice President of Preconstruction Scott Higgins has been analyzing the implications of COVID-19 on our projects since early January, before there was a pandemic. Initially, his goal was to anticipate how this global issue could affect our supply chain. Since then, Higgins has continued to research and evaluate the ever-evolving situation and what it means for our clients and partners, as well as our own business.

When it comes to advising on how to proceed, three of the most significant challenges facing those trying to write about COVID-19 are:

News and information are continuously changing.

Hard data is just now becoming available.

There is no precedence by which to compare.

Economists and financial experts are debating whether we will have a 'V' shaped recovery, a 'U' shaped recovery or a 'W' shaped recovery. Federal Reserve Chairman Jerome Powell has made several comments including calling all economic forecasts "highly uncertain." He also stated: "We are going to see economic data for the second quarter that's worse than any data we've ever seen." When you put all that into the soup kettle and start to stir, it begins to make more sense why there is not a lot of consensus about what kind of soup we will get in the end.

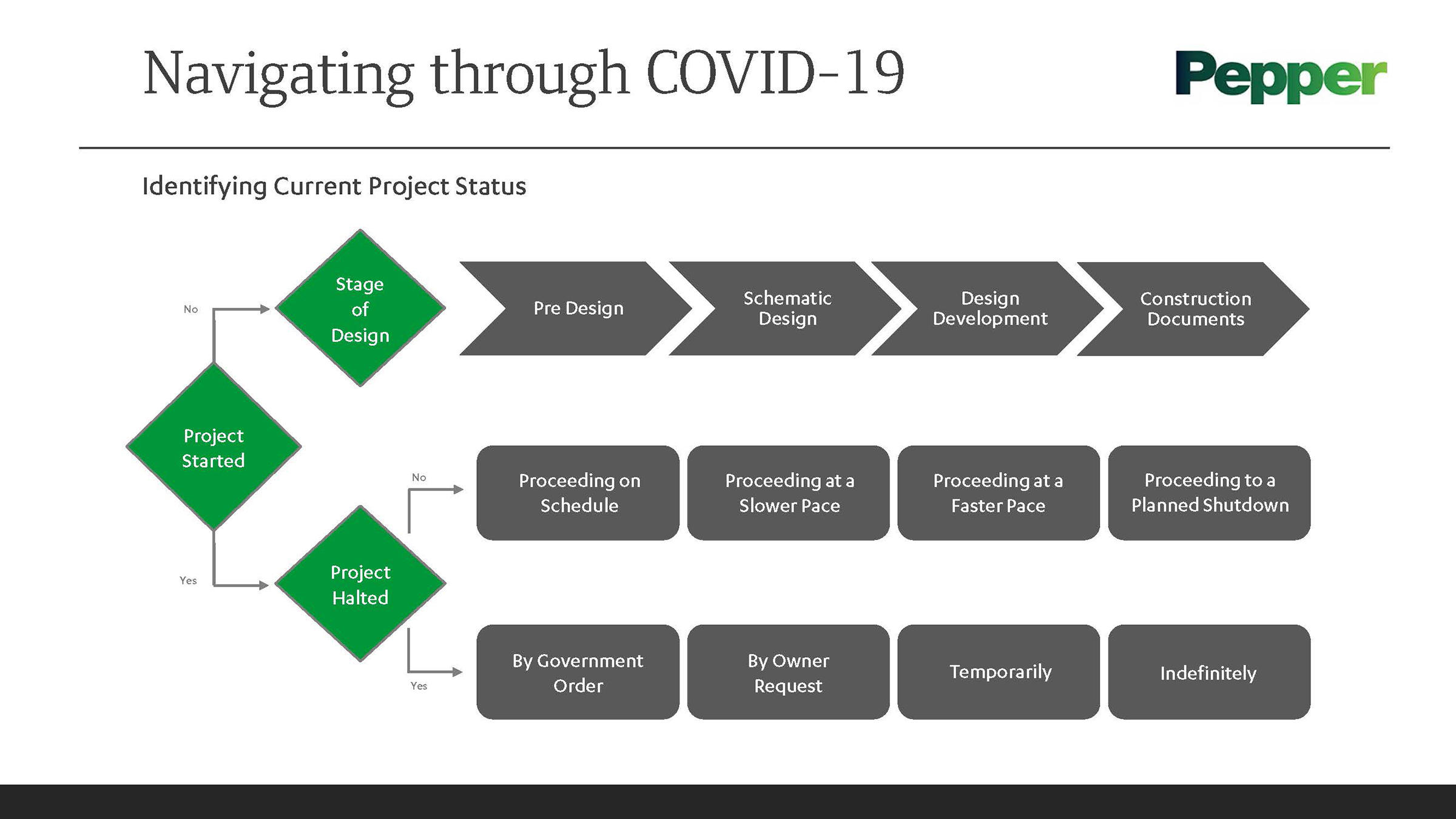

"Having grown up and worked in some fashion of the construction industry for over 40 years, I feel like I have insights to share," explains Higgins. "The two areas on which I have focused my career are cost and technology - and how to leverage their use to improve our processes. Something I have not seen in any of the articles I have read and researched is a process diagram to help navigate the current situation."

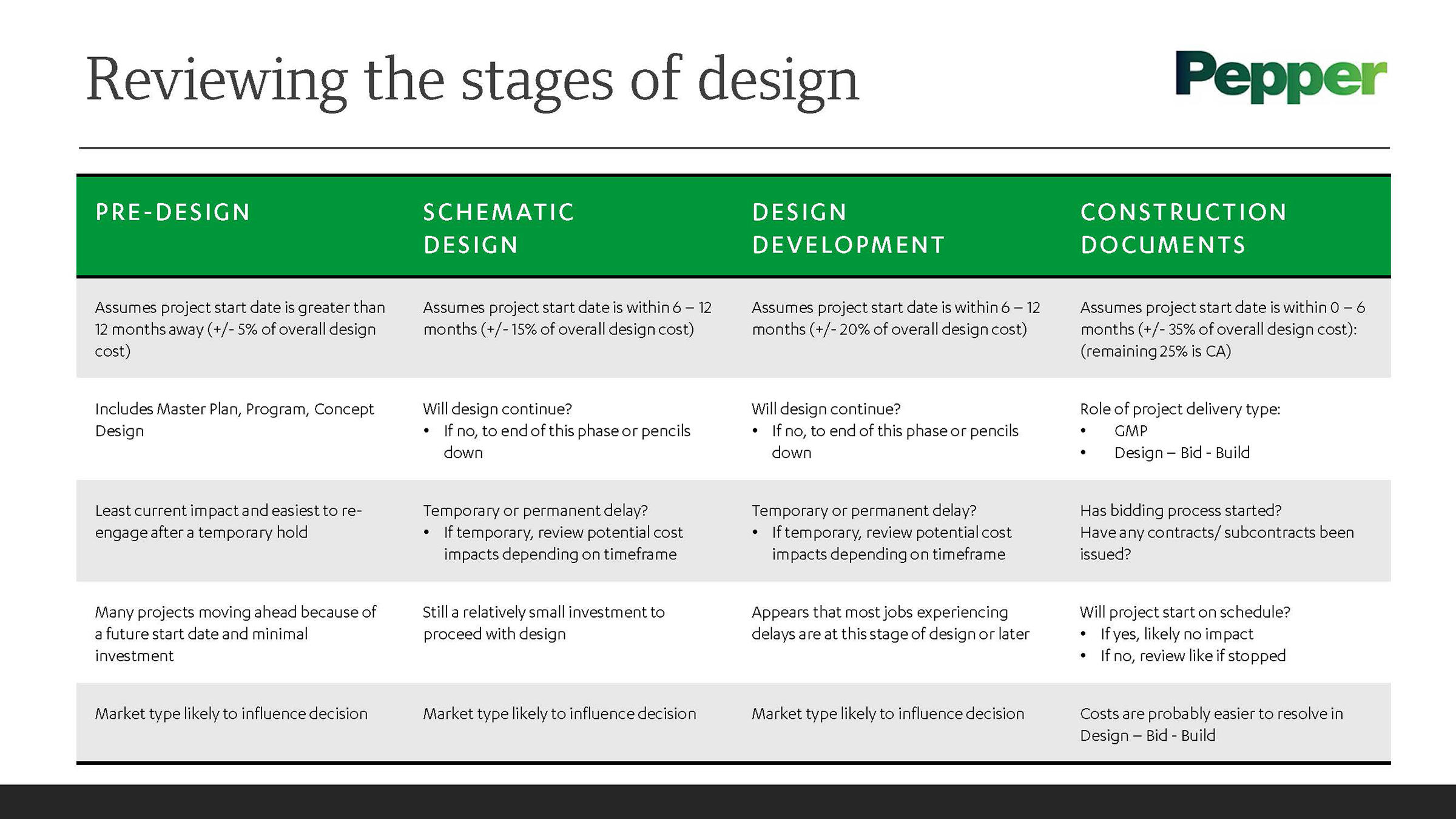

Evaluating the decision to proceed with a project

Some of the questions that need to be answered to plot a course for a specific project include:

Has construction on the project begun?

If so, has the project been stopped, slowed down, or otherwise impacted?

If not, what stage of the design process is the project currently in?

What type of building is it and what market does it serve?

Have any contracts or subcontracts been issued?

How will continuing, slowing down, postponing or cancelling the project impact end users in the short-, mid- and long-term?

What are the potential cost impacts to the project?

How can technology play a role?

Click on the image above for an overview of the decision-making process.

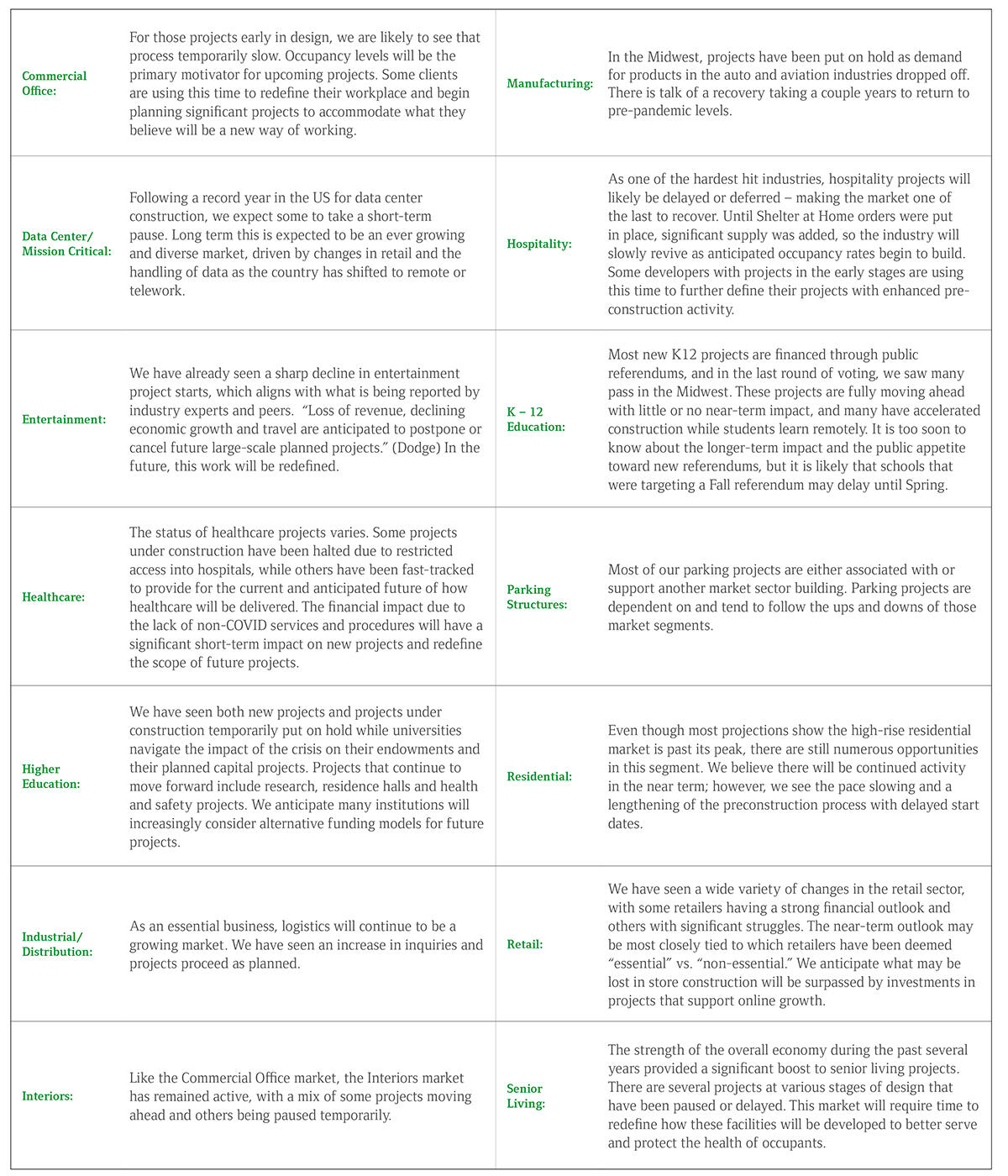

Looking at the differences of each market

The market segment, along with that market's corresponding overall economic outlook, is perhaps becoming one of the most significant pieces of data to consider. Not surprisingly, it's also an area where less information is available.

To help guide Pepper through the challenges that lie ahead, Senior Vice President and Chief Strategy Officer Jacqueline Lavigne has been keeping close tabs on how different markets are reacting alongside our pipeline of work. Her analysis has allowed our teams to approach conversations with clients from a more informed position.

"What we do know from speaking with our clients and monitoring our pipeline is that not all markets and geographies are being impacted equally. Sure, we've had recessions before," explains Lavigne, who has almost 30 years in the design and construction industry. "In addition to traditional macro-economic indicators such as GDP and unemployment statistics, we are closely monitoring how the construction industry is being impacted and looking for emerging geographic and market specific differences."

One of the lessons learned from the last recession was the importance of diversifying our work and monitoring our pipeline. Before the 2009 recession, healthcare was as much as half our volume. While it remains one of our primary markets, since then, we have seen many markets grow and contract across our offices. Today, our revenue is much more diversified across many markets, and as such, we are better prepared to help our clients and ourselves through the current situation.

"We've been doing Scenario Planning as part of our business for several years now, looking at leading indicators by overlaying the data from multiple sources: government statistics, the Dodge report, FMI and the Architectural Billing Index (ABI). During this crisis, we've added the Association of General Contractors (AGC) weekly survey. These go beyond the reports about job loss/unemployment claims, which are lagging indicators, and help us predict what to expect next." explains Lavigne.

Our approach factors in which scenarios have the highest probability of occurring. The chart above is just one of the many sources we use when planning for the future. Additionally, Higgins is part of an industry-leading Preconstruction Executives group from across the country who regularly discuss what they're seeing in the market.

While some impacts of COVID-19 are really apparent, in many sectors, it is still too soon to understand the full extent of the mid- and long-term effects the virus will have. As we have monitored industry data, local economies and talked with clients over the last quarter, we've observed the following market-specific impacts:

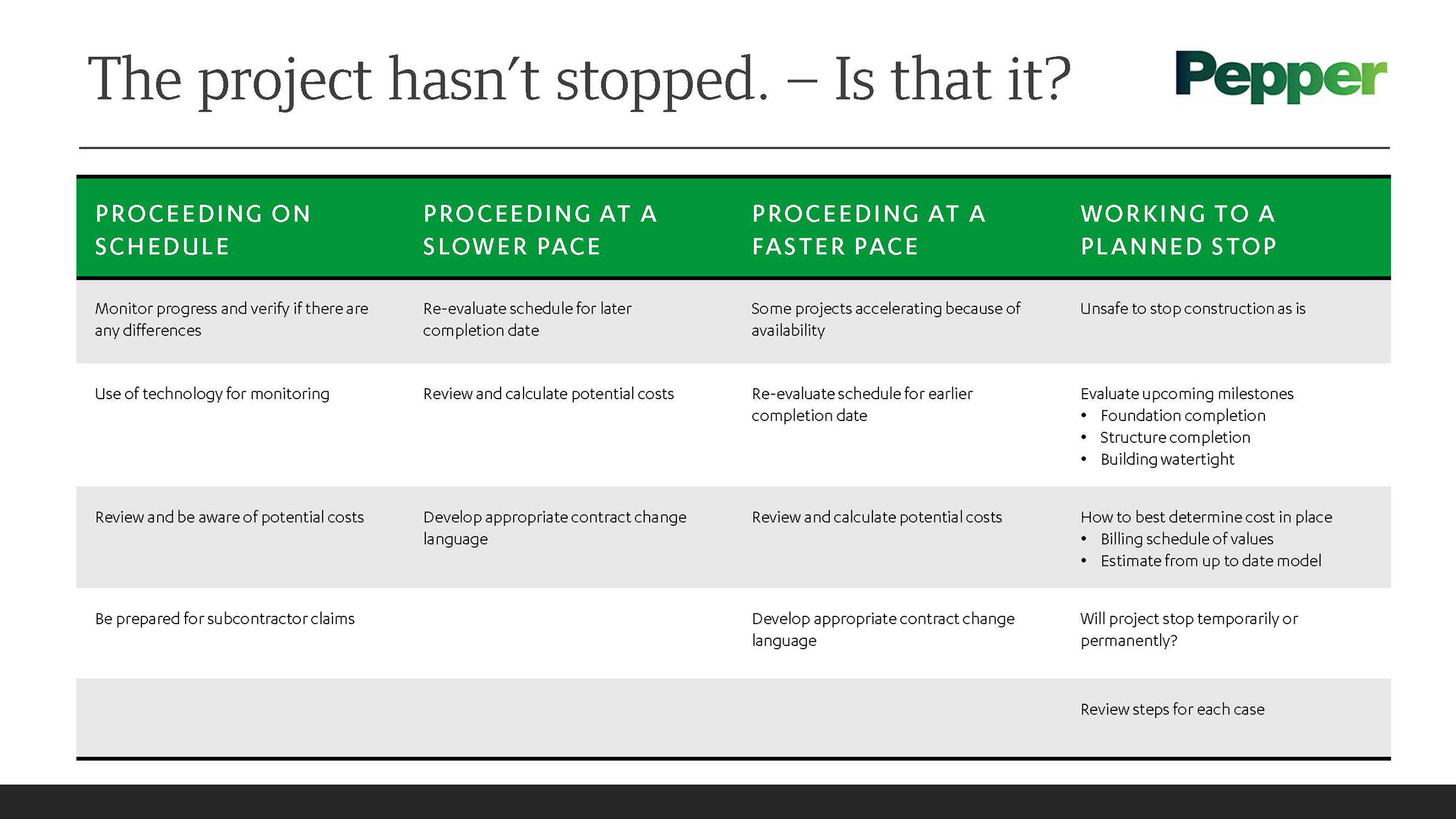

In many ways our projects and pipeline of opportunities confirm these projections; however, we also believe there is positive activity in each of our sectors, which doesn't show up in the aggregated numbers. Since we've started our analysis, activity continues to fluctuate. Owners most impacted have cancelled projects that were initially put on hold, which we anticipated. Others have restarted their projects earlier than originally indicated. Many developers have started asking for our advice whether now is a good time to start a new project. There may be a few premiums to build right now, but there are also several advantages.

Additional on-site costs of construction

There are some potential cost impacts for projects under construction that have not been stopped due to COVID-19, and they are relatively easy to quantify:

Workers stand six feet apart and wear masks during the daily huddle.

Costs associated with Personal Protection Equipment (PPE). These costs are mainly due to gloves, masks, face shields, protective suits, etc. Similarly, there are costs for properly disposing the used PPE, training in the proper use and disposal of PPE, and lost productivity from the additional training and use of PPE.

Costs associated with additional temporary procedures: barricades and partitions, trailers, tents and equipment required for jobsite entry testing and evaluation, additional cleaning, handwash stations, etc. and the safety training to mitigate new jobsite practices and procedures.

Cost impact of related absenteeism.

Costs for additional air filtration and purification.

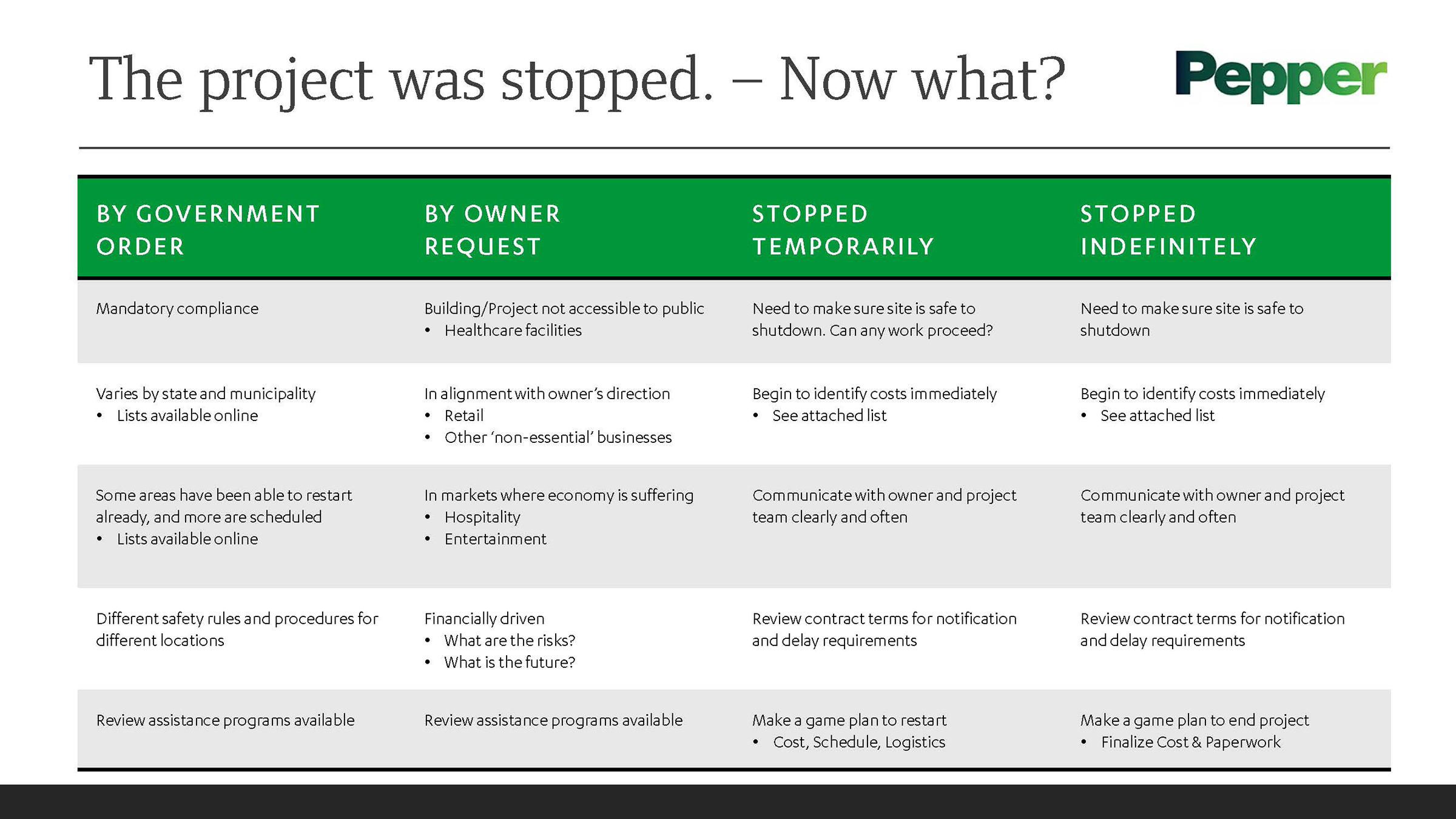

Costs of shutting down or delaying a project

There are also identifiable costs for project shutdowns and delays:

Cost of additional demobilization and remobilization.

Cost of minimal crew to monitor jobsite safety.

Cost of field supervision and project management staff during delay if applicable.

Potential costs for material management during delay.

Potential costs for future acceleration to recover lost workdays.

The future impact of a recession on construction

How we emerge from this crisis will be critical. Just as there are numerous ideas and projections about the type of economic rebound we will see as the pandemic subsides, there are many ideas and projections about the current and future cost impacts on construction.

The technical definition of a recession is two consecutive quarters of a reduction in GDP. There is little question that this is our reality and the eventual announcement will be a formality. The typical and historical impact of a construction recession is that costs go down quickly and return to pre-recession levels more slowly. That may or may not be the case with this recession. Part of the basis for this position is the nuance between cost and price, especially from a general contractor's point of view.

The difference between cost and price

Before the developer can make a decision to build, it's important to first understand the difference between cost and price and why price matters. The dictionary definitions of cost and price are interchangeable; however, the following example illustrates their difference for us. The cost of labor is expressed in so many $/hour. The cost of material is expressed in so many $/unit (cubic yards, square feet, lineal feet, etc.). For a subcontractor, the cost of work is primarily the sum of the cost of labor, material and equipment.

In scenario A, the subcontractor adds 15% for overhead and profit. In scenario B, the subcontractor adds just 5% for overhead and profit. As a general contractor the price paid for scenario B is 10% less than the price paid for scenario A. This is what typically happens in a recession. The cost of the basic inputs may not change at all, but the price paid can vary. The driver that most causes the price to change is the amount of competition vying for a reduced volume of work.

During the last recession we saw prices for work furnished and installed fall by as much as 10% to 15% or more because subcontractors removed overhead and profit from their bid proposals to generate cash flow. The cost of labor, especially in union markets, was constant at best and continued to rise over time. Material costs fluctuated but did not typically have the lasting impact of the change in overhead and profit. What potentially makes this recession different, is the underlying costs of labor and material may go up and provide a counter balancing effect to potential overhead and profit reductions.

Predicting the cost of construction

The focus of many stories in the news today is changing from the healthcare crisis to how the situation is broadly impacting supply chains. According to the American Iron and Steel Institute, domestic raw steel production at the end of April showed a decrease of over 39% from the previous year, and capability utilization dropped from 81% to 51%. There are stories with data like this across many types of manufacturing.

At this point, it's anyone's guess what will happen. The short-term effect is likely to be the immediate lowering of costs to keep in line with the sudden drop in demand. What is far from clear is what happens next.

In a sharp 'V' recovery, demand could rise much faster than manufacturing output can match, and the result would be higher costs for manufactured materials. Likewise, if significant numbers of skilled workers leave the construction industry in pursuit of other employment opportunities, there could be a significant labor shortage in a sharp 'V' recovery. These examples are less likely to be as impactful in a slower 'U' shaped recovery, and the supply of labor and material are more likely to keep pace with a slower increase in demand. If the recovery is 'W' shaped or some other more volatile pattern, the overall impact is much more difficult to predict.

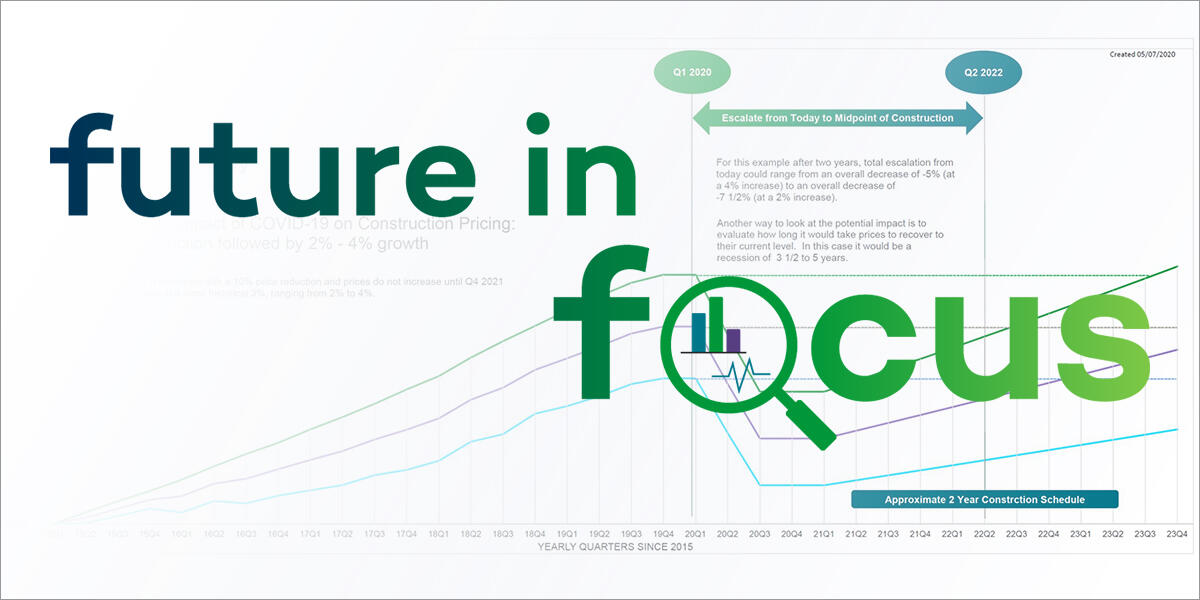

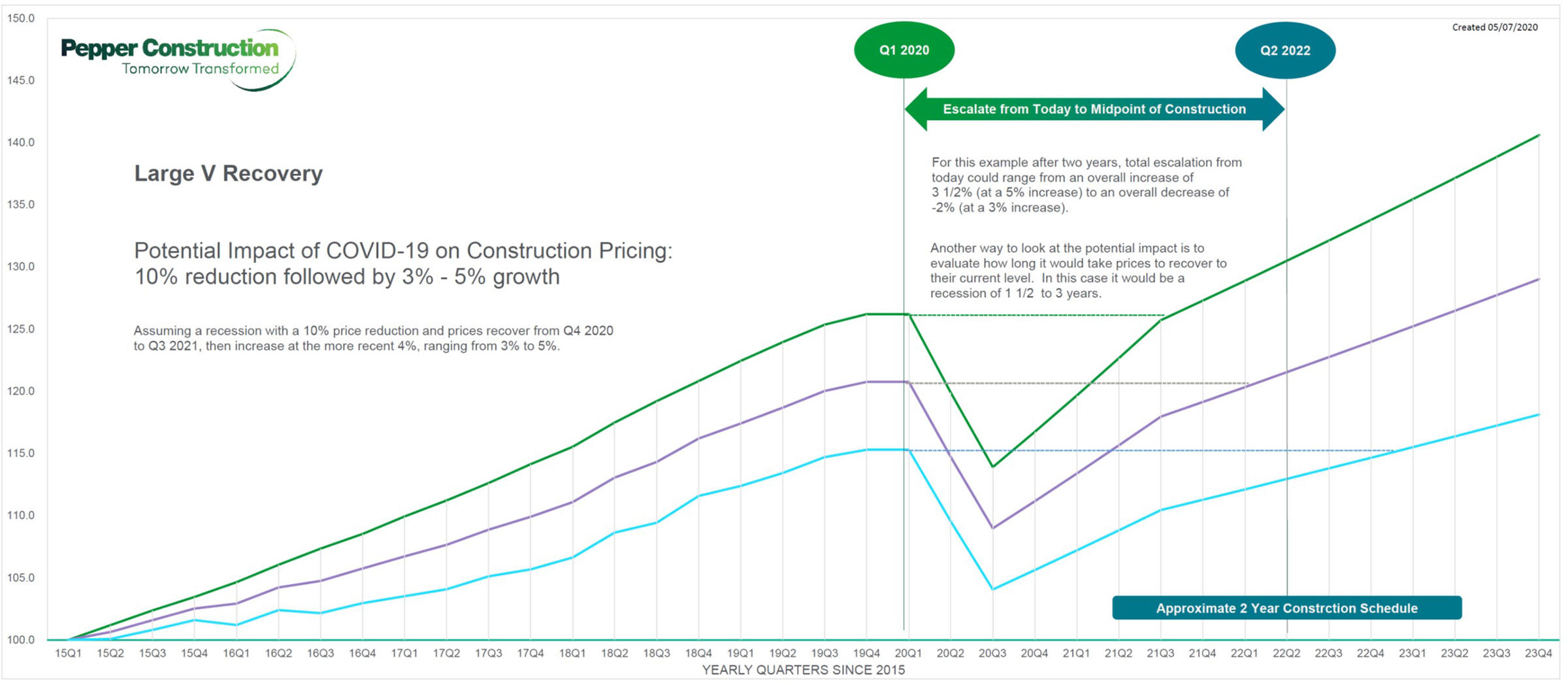

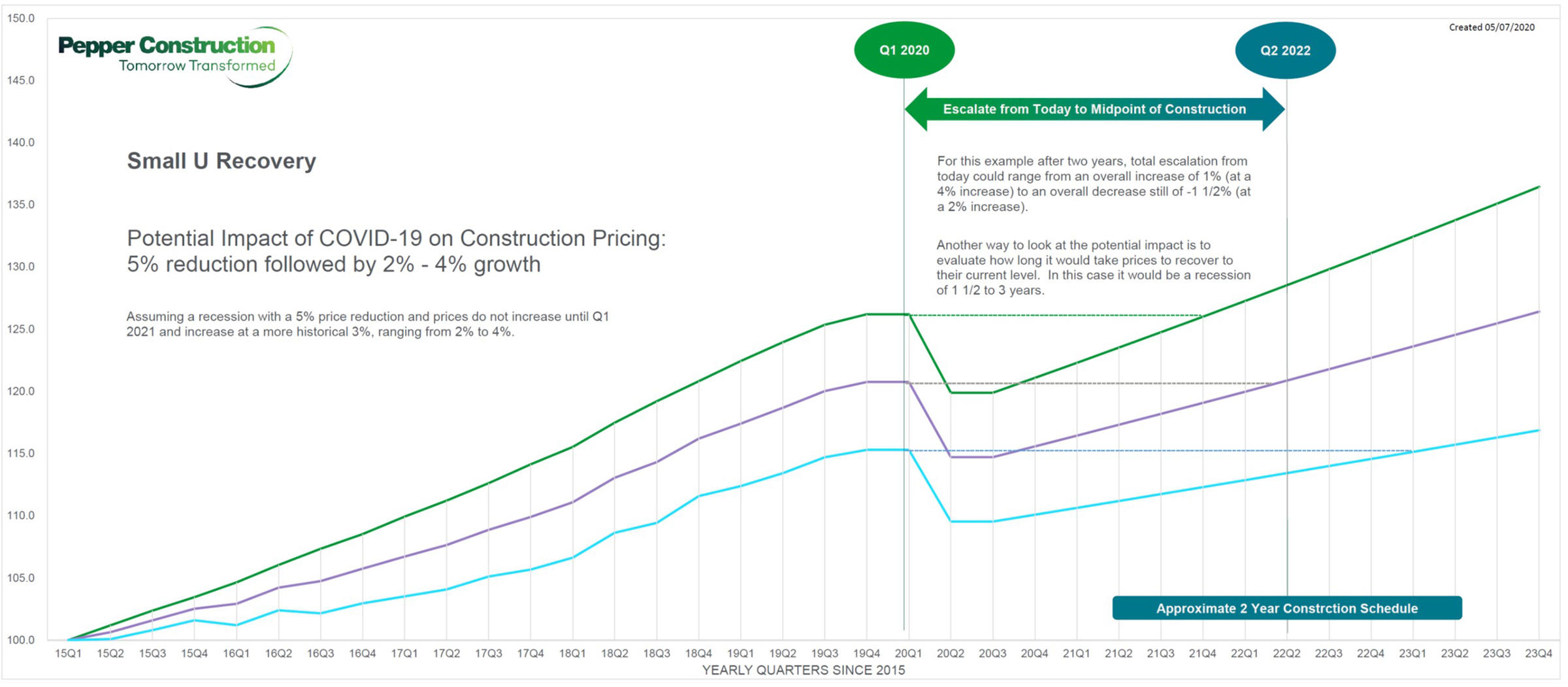

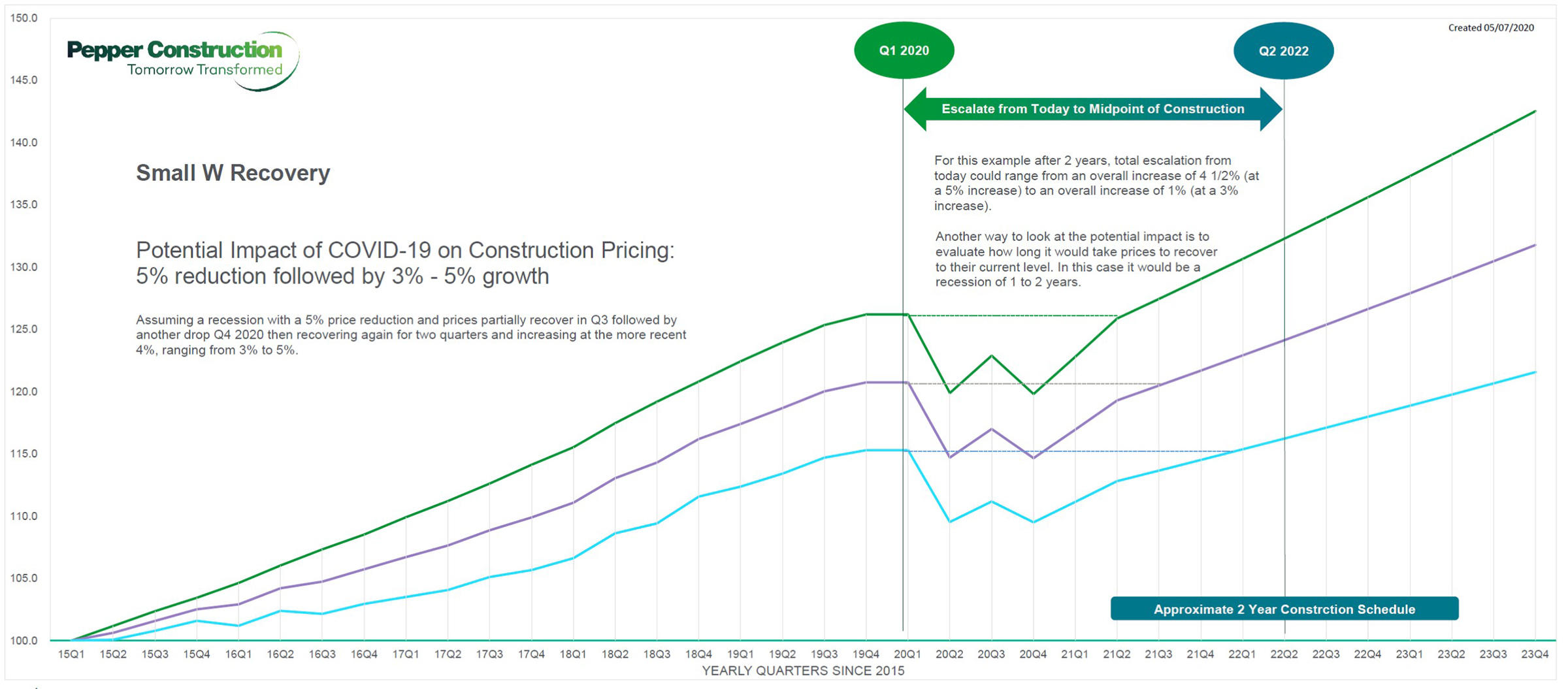

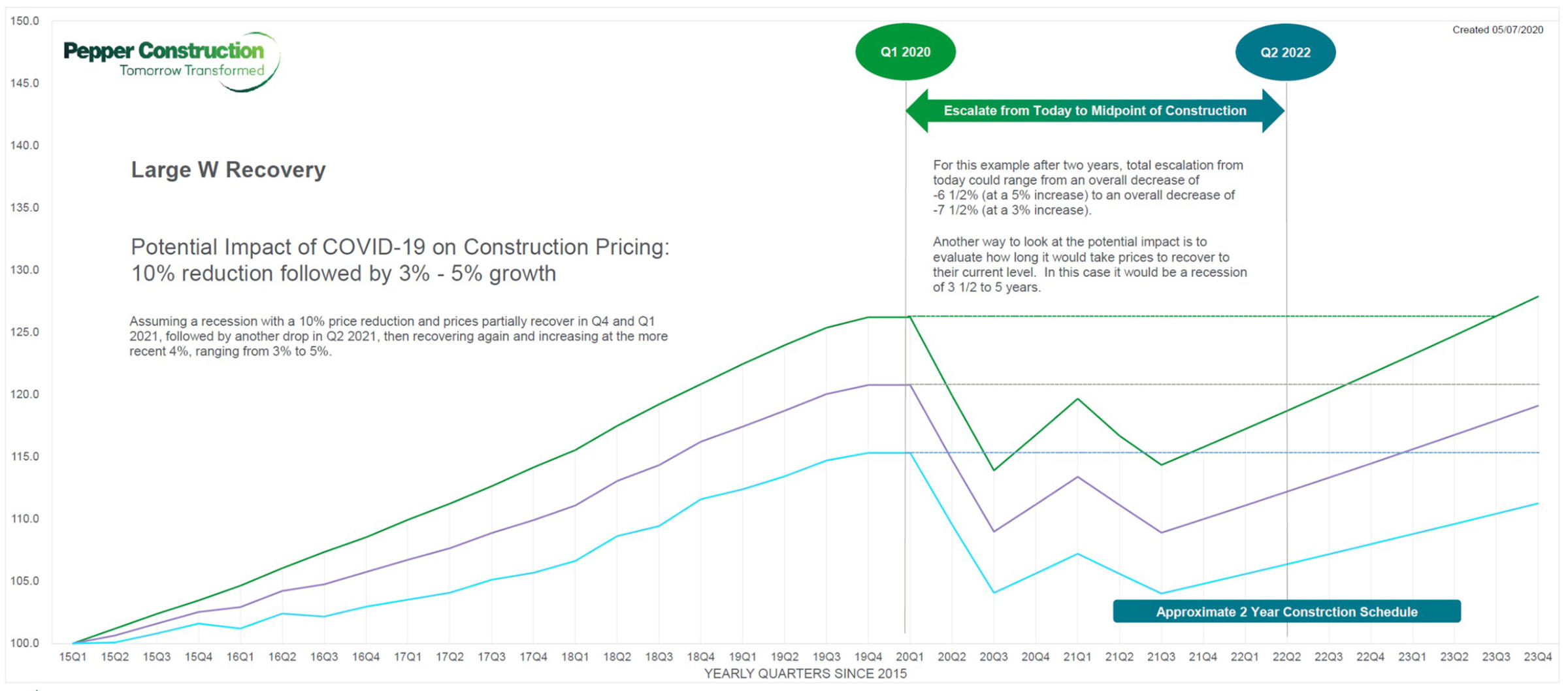

While many Cost Indices report on quarterly activities, based on our experience, we wanted to provide a look ahead because people build for the future. We've analyzed what could happen with construction pricing based on the economic models that have been suggested. He developed some graphical models to show what the pricing impact may be for each of the 'V', 'U' and 'W' recovery examples.

Click on the image to view the 6 recovery curves.

In each case we have assumed what both a 5% reduction in pricing and a 10% reduction look like.

Each model uses the same starting point of various historical tracking information that shows annual cost increases of 3% to 5% since 2015.

Each model looks at what the pricing impact could be on a hypothetical 2-year project that starts a year from now.

Each model also looks at the range of the length of the recession in terms of how long it would take for pricing to return to current levels with the stated assumptions.

The impact of both the 'large U' and 'large W' scenarios resemble what happened to construction pricing in the Midwest during 2009 to 2014 following the crash of 2008.

The following chart summarizes the information in the six graphic models.

Recovery Type

2-Yr Project Potential Escalation (Low)

2-Yr Project Potential Escalation (High)

Pricing Recovery Time Frame (Short)

Pricing Recovery Time Frame (Long)

Rank of Severity

'v'

2.5%

7.5%

1 year

1 ½ years

6

'V'

-2.0%

3.5%

1 ½ years

3 years

4

'u'

-1.5%

1.0%

1 ½ years

3 years

3

'U'

-7.5%

-5.0%

3 ½ years

5 years

2

'w'

1.0%

4.0%

1 year

2 years

5

'W'

-7.5%

-6.5%

3 ½ years

5 years

1

In recent days we have started to see an increase in the number of trade partners bidding on projects. This is a sign that either there is less work perceived as available in the near term, or there is significant fear that will be the case. We are also beginning to see some downward movement in the anticipated value of some trade partner bids, but it is too soon to tell what the magnitude of this may be. If these factors become a trend, it could be very similar to what we experienced at the beginning of the last significant recession.

Another potential impact on cost is the implementation by the federal government of the Payroll Protection Program (PPP) created by the CARES Act. The program allows small businesses (typically with less than 500 employees) to receive a grant or low interest loan based primarily on past payroll records. Without delving into the rules for either qualification or repayment a business with 30 employees could be eligible for approximately $500,000. If that business meets all the qualifications, the total amount would become a grant and not need to be repaid. For any portion that does not qualify, that amount becomes a 1% loan payable in two years. There could be scenarios where some contractors use this program for a competitive advantage. For some contractors that have not experienced a significant fall-off in workload, the PPP funds may be a way to lower pricing and not impact the overall bottom line. Even if a contractor that has to repay 100% of the PPP funds, a 1% loan is likely to be less than the current value of a contractor's line of credit.

There is a wide range of severity in the scenarios we tried to evaluate. Time will tell, and hopefully sooner rather than later, which is the most accurate.

So is now a good time to build?

Higgins responds: "Someone with a shovel-ready project would be able to secure value from the current economic conditions. We still expect to see higher competition and lower prices until the fear is gone."

Finding the right path forward

As discussed above, different market segments are experiencing different impacts. As the data becomes more available, we will share updated information.

One significant difference for us so far from the last recession is that preconstruction and marketing activities have remained high. Owners are still keen on receiving the best value for their investment and are not fixated on the lowest initial price through a lump sum bid procurement process.

"This is good news for us and for our clients," commented Lavigne. "When we walk through the preconstruction process together, we are better able to help owners make the most informed decisions for the life of their building and advance their project by making turnkey decisions before ground is broken."

This blog post is part of a new series that analyzes the decision to proceed, as well as the creativity and tools to wisely manage your project. Experts from across the company will weigh in so you can start to sort through all the unknowns and make the most informed decisions possible. The next post in our series will share how to get more value out of work that is proceeding by looking for efficiencies and leveraging technology. After that, we'll take a deeper dive into some specific markets to better understand what's driving them, where they are headed and how to think differently about your project during this time. We encourage you to subscribe to our newsletter to receive updates.

SIGN UP TO RECEIVE UPDATES

About the Authors

Scott Higgins, LEED APSenior Vice President of Preconstruction

As senior vice president, Scott provides leadership for Pepper’s Centers of Technical Excellence. With 30 years of experience, Scott provides some of the industry’s most compelling thought leadership in the disciplines under his guidance. His expertise leads to compelling solutions and counsel for the most discerning clients, drawing on his years in self perform work, estimating and project management. Scott holds a Master of Science in Civil Engineering and a Bachelor of Science in Construction Engineering from Iowa State University, and he is a LEED AP.

Jacqueline Lavigne, LEED® AP Chief Strategy Officer

As chief strategy officer for Pepper Construction Group, Jacqueline helps establish the company’s growth strategy. Her responsibilities include marketing, business development, public relations, communications and content development, as well as facilitating Pepper’s strategic planning activities. Jacqueline has also provided strategic expertise on projects through kick-off and team-building strategies, which particularly benefit teams with shared agreements.

Jacqueline has 35 years of experience in the industry, including extensive experience in business and market planning and analytics. Before joining Pepper, she served as chief marketing officer for NELSON and as marketing principal for global architecture firm HOK. She holds a Master of Architecture from North Carolina State University and is a LEED Accredited Professional.

Jacqueline is dedicated to the Ride Janie Ride Foundation, which assists individuals facing financial hardship resulting from ongoing medial treatment of various types of cancer. She is also a longstanding member of the City Club of Chicago.

Skip to main content

Skip to main content